With so many unknowns, a BYU dean—and household finance expert—shares pointers to help gain stability.

Cynthia (name changed) has been living on disability income for several years now, barely getting by. After suffering deep financial losses in the Great Recession a decade ago, going through a difficult divorce, and developing medical problems, she had finally begun to think her finances were looking up. But the last few months have added new layers of stress, uncertainty, and diminished hope of ever digging out of her financial hole. “Now, the very fragile lifelines that I rely on are under more threat and are more beyond my control than ever,” she says.

Cynthia started out the pandemic at a disadvantage, like many other individuals and families. While some might be feeling secure, most of the population is dealing with daily stress, brought on by the number of unknown variables swirling and intersecting unpredictably. Will I get sick? Will a loved one get sick? Will they die? Will I lose my job? Will I be able to find a job? How long can I go without income? What if I die?

Brigitte Condie Madrian (BA ’89, MA ’89), dean of the BYU Marriott School of Business and an expert in household finance, thinks COVID-19 has at least one silver lining: “We don’t have as many activities and gatherings and trips, so a lot of people have more time on their hands. That’s not true of everyone, but for those with the extra time, it’s an opportunity to spend it on things that often take a back seat to more immediate activities, things like how to get yourself in a good financial position.”

Madrian offers several recommendations for those navigating the new normal of living with an ongoing pandemic in the United States. (If you live outside the United States, many of the basic principles she discusses still apply.)

Be Cautious with 401(k) Loans

Not everyone has a 401(k), but if you do, the CARES Act (the financial relief bill recently passed by the U.S. Congress) makes it easier to take money out for financial hardship. “The catch is that you have to pay it back over three years or end up paying taxes if you’re under 59.5,” says Madrian. If you’ve been adding to your 401(k) for a while, your nest egg might look like a lot of money, and it can be tempting to take out more than you really need. “Just as it’s hard to eat just one potato chip, it’s hard to take out just a little from your 401(k). You’re better off leaving it alone if you can,” she says.

Consider Refinancing Your Home

For those who own a home, now is a good time to refinance as interest rates fall. However, cautions Madrian, too often, homeowners who are refinancing are tempted to also take cash from their equity. “If you don’t need cash, leave your equity alone. If you lost your job and need cash, refinancing is a way to tap into some of your home equity while also reducing your household costs, but keep in mind that repaying will be more difficult without a job,” she warns.

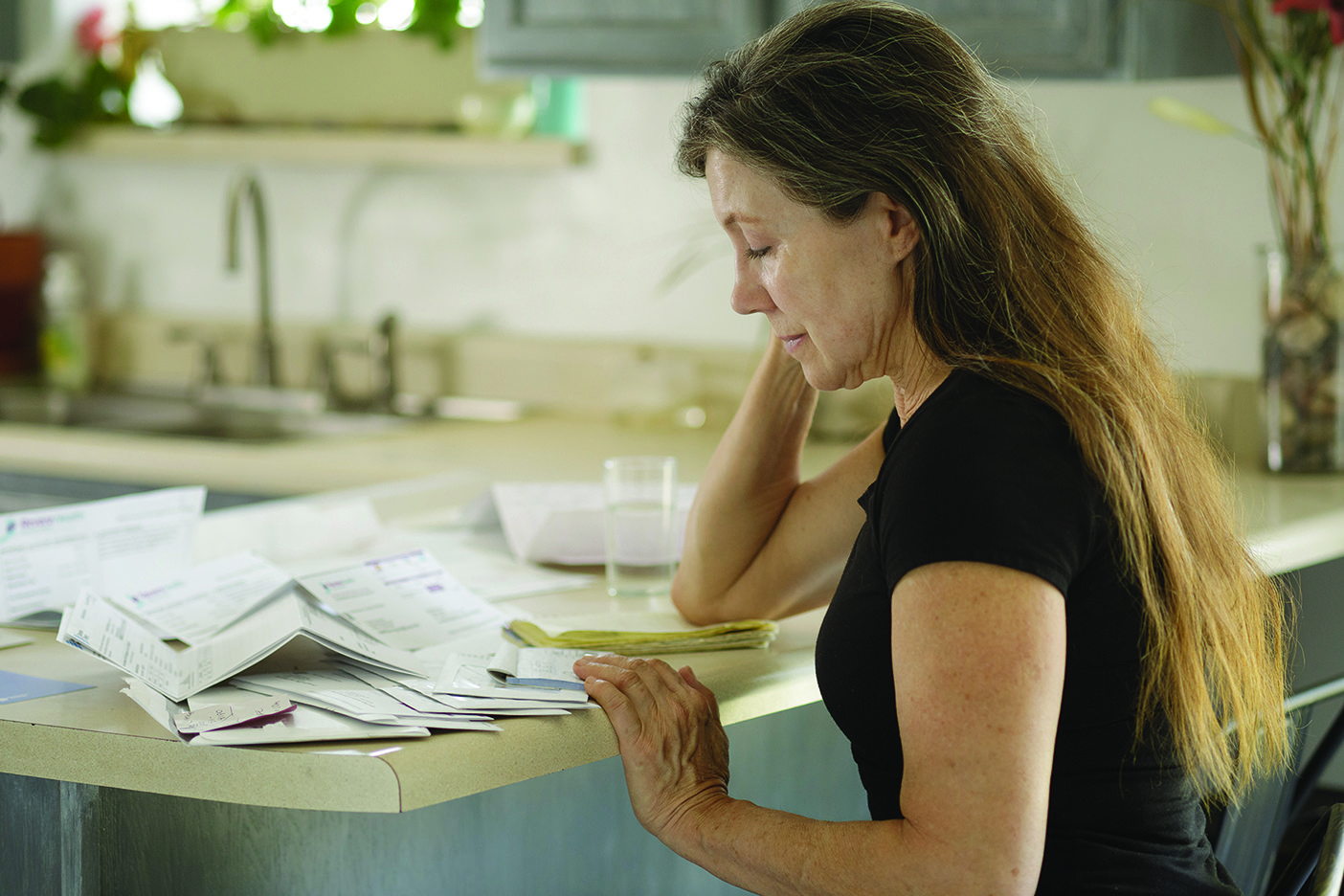

Save Part of Your Stimulus Money

A widely reported 2018 survey of 1,000 Americans showed that almost half don’t have enough in liquid savings to cover an emergency like a major car repair or a flooded basement. Among millennials (defined by the survey as ages 22 to 37 in 2018), almost 60 percent don’t have enough.

Rainy-day funds are a critical antidote to financial—and emotional—breakdowns. Madrian suggests that if you don’t need all of the stimulus money you received from the government, save part of it toward an emergency fund. “Spend some of it so you contribute to the intended purpose—stimulating the economy—but don’t spend all of it if you can avoid that,” she says. If you’ve had to spend down your rainy-day fund, start building it back up as soon as you can.

Resist Paying Attention to Stock-Market Volatility

When the stock market is swinging wildly, many people are tempted to either reduce the amount they’re saving or change their investment allocation so that less is in the market. But most people are bad at timing the market, says Madrian. They tend to sell after prices have already dipped and the market is starting to recover. “By the time they get back in, they’ve missed out on all the increase—after suffering all the loss,” she says. “In general people are better off if they adopt a long-term investment strategy and just stick with it.”

Review Your Insurance Coverage

The younger you are, the less likely you are to think carefully about life insurance. Madrian believes that once COVID-19 deaths go down, we’ll begin to hear more about families left financially vulnerable because the breadwinner died and didn’t have life insurance. People don’t like to think about death, but Madrian says breadwinners with dependents, regardless of age, should ask themselves, “If I were to get sick and die, would my family be financially taken care of?”

Madrian also recommends that those who have disability insurance through their jobs review their coverage. And adults dependent on others’ income should learn about government survivor benefits as well as survivor benefits through their breadwinner’s employment or life insurance. It is important to make sure beneficiaries are accurate and up to date.

Stay Hopeful Despite the Challenges

With oversight of thousands enrolled in the Marriott School, Madrian is seeing students and new graduates under a lot of stress. They have very little savings or none at all, and many can’t earn the summer income they were planning on to pay tuition and living expenses for the fall. New graduates have had offers rescinded or start dates pushed back. “They’re feeling a lot of stress financially. Part of it comes from not having lived through a previous financial crisis as an adult—not having the confidence and experience that they’ll make it through this,” she says.

To all those unemployed because of the pandemic, Madrian says, “Now is a good time to further invest in yourself. A lot of great online classes have become free, and you can develop skills that will make you more attractive as a job candidate. Don’t give up hope. It’s tough but you’ll make it.”

Even veteran survivors of multiple financial setbacks can become discouraged despite their seasoned experience, as Cynthia knows well. “Job loss, career loss, health loss, spouse loss, parent loss—so much loss,” she says. And yet, she considers herself among the lucky ones. “I’m still alive, my brain still mostly works, my kid loves me, we have a safe place to live and food in the pantry. That hasn’t always been true, and I’m beyond grateful.”

Counter Stress Eating with Nudge Theory

People under stress tend to engage in unhealthy behaviors in an attempt to escape their problems or to feel numb. “We do things that are comforting. We sit on the couch and eat more chips. We stress bake and stress eat,” says Madrian.

Part of her research includes health behavior and how it can be changed to improve health outcomes. She says most people don’t change their behavior even with data that says they should or with a desperate desire to change.

“Nudge theory” can help. It’s the idea that intentionally setting up our physical environment can move us toward better choices. Here are a few nudges Madrian suggests to boost your health as you cope with the pandemic:

• If you’re working from home and are tempted to snack more than usual, set up your office as far away from the kitchen as possible. Make it harder to sneak whatever you’re craving.

• Put your workout clothes on first thing and wear them until you exercise.

• If you’re sitting a lot, set a timer to go off every hour. Get up for a few minutes and move around in a way you enjoy, such as playing with a pet, moving to music, or accomplishing a brief task like watering a plant.

• Your nudges won’t work all the time, so don’t expect them to. Keep tinkering with your nudges to see what helps and what doesn’t.